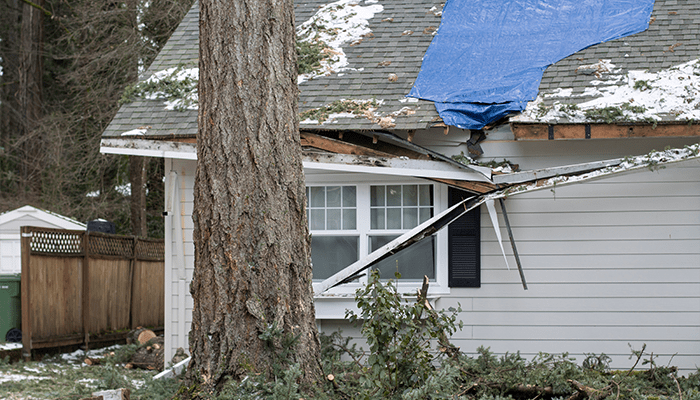

Hurricanes can be devastating and cause significant damage to your home and property. To minimize the potential for catastrophic losses due to hurricanes, many homeowner’s insurance policies that provide windstorm coverage have a separate deductible for hurricane windstorm losses.

As an example, the Florida Office of Insurance Regulation states that the hurricane deductible applies only if the windstorm damage occurs during a hurricane named by the National Hurricane Center of the National Weather Service. Hurricane deductibles apply for damage that occurs from the time a hurricane watch or warning is issued for any part of Florida, up to 72 hours after such a watch or warning ends and anytime hurricane conditions exist throughout the state.

The separate deductible applies for a calendar year (January 1 to December 31) and only once during a hurricane season. After the hurricane deductible has been met, it no longer applies to any subsequent covered windstorm losses after a hurricane watch or warning has been issued. Instead, the All Other Perils deductible will apply for each subsequent loss.

Insureds should be mindful that all expenses are subject to this deductible, even emergency repairs. Insureds are required to make emergency repairs in order to prevent further loss. It is important for homeowners to maintain proof of any expenses incurred for any hurricane damage, even if it is under their deductible, as they can use it to satisfy the deductible should more than one hurricane claim occur in the calendar year.

How much is a hurricane deductible?

Depending on your individual policy, hurricane deductibles are either a fixed amount or a percentage of your home’s Coverage A amount (e.g., 2% of $200,000 = $4,000). This deductible is for windstorm coverage. Your deductible amount will be subtracted from the amount of any loss or claim payment you receive.

The states that have hurricane deductibles include: Alabama, Connecticut, Delaware, Florida, Georgia, Hawaii, Louisiana, Maine, Maryland, Massachusetts, Mississippi, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South Carolina, Texas, Virginia and Washington DC. For help with deductible reviews on your insurance policies, visit AssuredPartners Personal Insurance.

Source: Insurance Information Institute